Toss / Viva Republica Deep Dive 2026: Korea's Fintech Super-App Company

A public-info deep dive on Toss and Viva Republica, covering its super-app model, user reach, fintech ecosystem, risks, and global lessons.

Quick Answer

Toss is worth studying because it turned a narrow Korean consumer pain point, simple money transfer, into a broad financial interface. Viva Republica Inc., the company behind Toss, now presents Toss as a financial super app that connects spending, transfers, credit-score tools, loans, securities, payments, insurance, merchant services, and business tools in one mobile experience.

For overseas readers, the useful point is not that every market should copy Toss feature by feature. The useful point is that Korea became a test case for a UX-led fintech company operating inside a highly regulated, bank-heavy, mobile-first market. Toss shows how a company can use one high-frequency trust moment, sending money, to build a wider financial habit.

![]()

This is a public-information-only company spotlight. EpicKor is not implying a client relationship with Toss or Viva Republica, and this article is not investment advice. The goal is to explain why the company matters, what public information says as of July 2026, and what overseas operators should verify before drawing conclusions from the Toss model.

Why Toss Matters Outside Korea

Korea is a useful market for fintech observation because the country combines dense mobile usage, fast consumer adoption, strong incumbent banks, active securities participation, card-heavy payments, and strict financial regulation. A product that becomes habitual in that environment has usually solved more than a design problem. It has solved trust, compliance, onboarding, data, partnerships, and reliability problems at the same time.

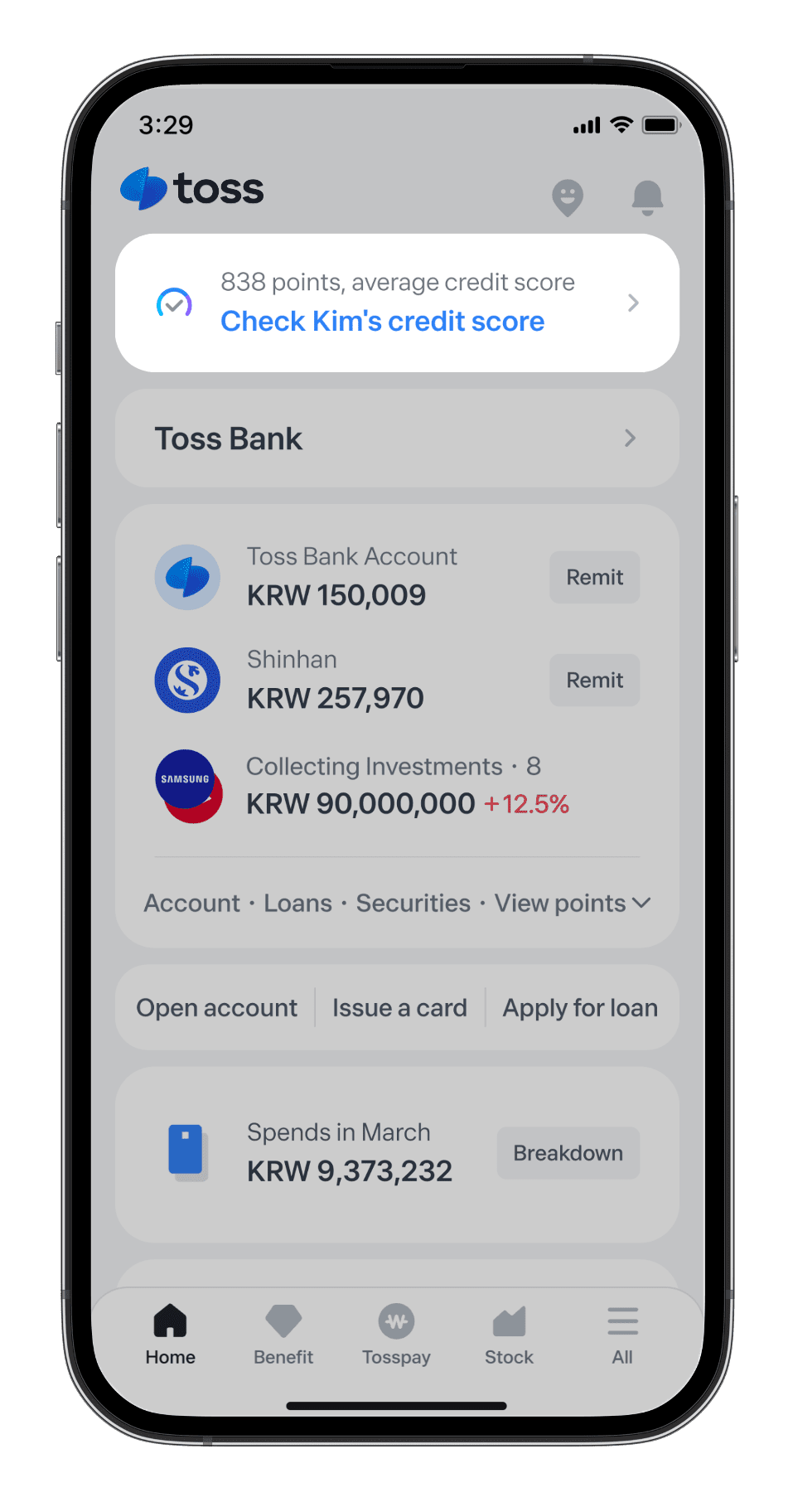

Toss began with a simple transfer experience and expanded into a broader financial surface. The company's own English pages describe Toss as a platform for managing a user's financial life, including bank accounts, cards, insurance, securities accounts, spending, credit scores, loans, investing, payments, taxes, verification, and business tools. The official team page also identifies Toss as Korea's leading financial super app and says it is used by more than one in two Koreans.

For operators, that makes Toss interesting in four ways.

First, it shows how a fintech product can use one daily action as a wedge. Transfers are not glamorous, but they are frequent, personal, and trust-heavy. If the product can make that action easier and safer, the app earns permission to handle more financial decisions.

Second, Toss shows how interface design becomes strategy. The company is not only competing on interest rates or fees. It competes on whether the user can understand a financial task quickly enough to act.

Third, Toss is a case study in regulated ecosystem building. Its product surface includes banking, securities, payments, insurance, advertising, and merchant tools. Those are not one product line; they are several regulated or partner-dependent lanes.

Fourth, Toss is useful for overseas companies studying Korea because it reveals where Korean consumers have become comfortable with financial aggregation: checking credit scores, comparing loans, investing inside a familiar app, using mobile payment rewards, and treating financial management as a continuous app experience rather than a branch visit.

What Toss Actually Does

Toss is best understood as a consumer and merchant financial stack rather than a single app utility. The public pages group the service around user money management, transfer, loans, credit score, securities, insurance, payments, and business tools.

| Layer | Public Toss Surface | Strategic Meaning | What To Verify |

|---|---|---|---|

| Daily finance | Spending, account aggregation, financial dashboard, transfers, credit-score tools. | High-frequency usage creates habit and trust before bigger financial decisions. | User engagement, retention, fraud controls, and whether users keep Toss as their default money app. |

| Marketplace finance | Loan comparison, credit cards, insurance inquiry, personalized financial offers. | Toss can turn attention and data into matching, recommendation, and referral surfaces. | Commission structure, suitability controls, consumer-protection process, and partner concentration. |

| Regulated subsidiaries | Toss Bank and Toss Securities sit around banking and investing use cases. | The brand stretches from interface layer into licensed financial services. | Disclosures, capital strength, risk management, compliance history, and product-level profitability. |

| Commerce and merchants | Toss Pay, Toss Payments, Toss Checkout, Toss Place, and business dashboards. | The company can serve both the consumer side and merchant operating side of payments. | Merchant adoption, payment reliability, fee competition, dispute handling, and offline POS execution. |

| Data and advertising | Official materials describe business advertising driven by financial data. | Financial attention can become a targeted business-customer channel if privacy and trust are protected. | Consent design, privacy controls, ad quality, regulatory scrutiny, and user trust. |

The important distinction is that a super app is not just a long feature list. A financial super app has to make many financial tasks feel coherent while keeping each regulated product legally and operationally separate where required. That is the hard part.

From Simple Transfer To Financial Habit

Toss says its first simple transfer service launched in February 2015 without requiring an accredited certificate. That matters because Korea's older online finance experience was often fragmented across certificates, plug-ins, bank apps, and confusing user flows. Toss found a consumer pain point that almost everyone could understand: sending money should be simple.

The company's 10-year data report says the figures in that report are based on accumulated data from launch through November 2024 unless a specific period is separately indicated. Its official team page says registered users among Koreans in their 20s reached 5.5 million, 30s reached 5.6 million, and 40s reached 5.7 million, with the percentages based on Statistics Korea population data and Toss user data as of December 2024.

Those figures are useful because they suggest Toss is not only a Gen Z app. The public age-group metrics imply multi-generation adoption across Korean adults. For a financial app, that matters. Broad adoption makes the product more useful as an operating layer because each additional feature can be introduced to an audience that already has some trust in the brand.

The more interesting lesson is sequencing. Toss did not start by asking users to accept a full financial universe. It solved a painful task first, then expanded into related trust moments: checking credit, comparing loans, investing, managing spending, paying merchants, and handling business payments.

The Current Toss Ecosystem

The current Toss story is broader than Viva Republica alone. Toss Bank has its own public site and disclosure area. Toss Securities has its own official service surface. Toss Place addresses offline stores through POS-style merchant tools. Toss Payments and Toss Checkout sit closer to online commerce. Together, those products make Toss a network of financial experiences around one consumer brand.

![]()

This ecosystem gives Toss several possible advantages.

One advantage is cross-context recognition. A consumer who already uses Toss for transfer or credit score may be more willing to try investing or payment tools inside the same interface. A merchant who sees Toss as a payment brand may be more open to a Toss checkout or POS product.

Another advantage is data and personalization. Financial products become more useful when recommendations are timely and relevant. The risk is that the same data power can create privacy, consent, and trust concerns if the user feels the product is too intrusive.

A third advantage is brand compression. Korean finance can feel fragmented across banks, brokerages, card companies, insurance companies, payment providers, and verification systems. Toss tries to reduce the user's cognitive burden by making many tasks feel like one experience.

The downside is complexity. Each additional layer brings a different regulatory, operational, and reputational risk. Banking risk is not the same as securities risk. Payments reliability is not the same as advertising ethics. Insurance inquiry is not the same as loan matching. The wider Toss becomes, the more the company has to protect clarity.

Operator desk note: As an Amazon Associate, EpicKor may earn from qualifying purchases. If you are studying Toss as a product strategy case, compare fintech strategy books and financial-services product management books before mapping the model to another market.

The Business Model Lens

Toss should not be reduced to "an app with many features." The stronger lens is a layered model.

At the first layer, Toss owns attention around daily financial actions. That layer has to feel fast, safe, and low-friction.

At the second layer, Toss can match users to financial products: loans, cards, insurance, investment services, and other offers. This is where recommendations and marketplace economics become important.

At the third layer, Toss-linked businesses can operate licensed or specialized services, such as banking, securities, payments, and merchant tools. This is where revenue opportunity can grow, but regulatory and risk-management demands rise.

At the fourth layer, Toss can serve business customers through payment infrastructure, checkout UX, merchant dashboards, POS devices, and advertising. This makes the company relevant not only to consumers but also to Korean commerce operators.

The broad lesson for overseas founders is that a super-app strategy usually needs a trust wedge, not only a menu. Without a high-frequency trust wedge, a finance app becomes a folder of unrelated tools. With a wedge, each new feature can attach to a habit the user already understands.

What Overseas Operators Should Not Copy Blindly

Toss is attractive as a case study, but copying it directly can be dangerous. Korea's market conditions are specific.

Korean users were already comfortable with mobile payments, fast identity verification, online banking, and app-based daily life. Korea also has concentrated financial incumbents and a dense urban consumer base. A market with lower bank penetration, weaker digital ID rails, or different regulatory rules may not respond the same way.

The regulatory path is also market-specific. A simple transfer feature, credit-score tool, banking product, securities flow, and payment checkout can each require different licenses, partnerships, disclosures, and consumer-protection controls. In many markets, the fastest interface idea is not the safest legal path.

Finally, brand trust travels slowly. Toss earned trust through repeated small financial moments. A new entrant cannot shortcut that by launching many products at once.

Risk And Future Watchlist

The future of Toss depends on whether it can keep the interface simple while the company behind it becomes more complex. That is the central tension.

| Watch Area | Why It Matters | Signal To Track |

|---|---|---|

| Regulatory scrutiny | Finance expansion increases exposure across banking, securities, payments, credit, insurance, advertising, and data use. | Public disclosures, regulator notices, consumer-protection updates, and product-rule changes. |

| Trust and security | A finance super app depends on users believing the app is safe enough for daily money decisions. | Fraud-prevention features, security incidents, complaint handling, and account-protection communication. |

| UX complexity | The product promise weakens if the app becomes crowded or confusing. | Navigation changes, user reviews, feature bundling, and whether high-frequency tasks stay fast. |

| Subsidiary performance | Banking, securities, and payments products can carry different cost, capital, and risk profiles. | Management disclosures, product profitability, capital metrics, and risk commentary where available. |

| Competitive response | Korea has strong banks, card companies, platform companies, and payment providers. | Bank-app redesigns, platform-finance launches, merchant-fee competition, and exclusive partnerships. |

The upside case is clear: Toss keeps its consumer trust, adds more useful regulated services, and becomes a default interface for Korean personal and merchant finance. The risk case is also clear: broader services create more operational drag, more regulation, and more chances for users to feel the app is no longer simple.

What Buyers, Partners, And Researchers Should Check

If you are an overseas operator studying Toss for partnership, market entry, product design, or Korea research, use a checklist rather than a headline.

Start with the official Toss pages for product scope and adoption claims. Then separate Viva Republica, Toss Bank, Toss Securities, Toss Payments, Toss Place, and other related surfaces where relevant. Each entity and product lane may have different disclosures and operating constraints.

Check whether the public numbers you are using refer to registered users, active users, transaction volume, sales, gross merchandise value, or cumulative activity. These terms are not interchangeable. A company can have very strong registered-user numbers while product-level economics vary by category.

For a partnership angle, identify the exact business surface. A merchant payment integration is different from consumer acquisition. A data or advertising partnership is different from a bank product. A securities or investment partnership is different again.

For a product strategy angle, study the sequence: pain point, trust, habit, expansion. The sequence is more transferable than any single feature.

Research kit: If you are building a Korea fintech briefing, compare Korea business books, startup strategy books, and business research notebooks so your source notes stay separated by product, entity, and date.

Practical Lessons From Toss

For founders, the core lesson is that the wedge matters. Toss did not become interesting because it declared itself broad. It became interesting because it made one financial task feel easier and then used that trust to expand.

For product teams, the lesson is that regulated UX is not decoration. When money, credit, identity, or investing is involved, simple language and a clean interface are part of risk control.

For Korea-market researchers, Toss is a reminder that Korean consumers can adopt new financial interfaces quickly when convenience, trust, and official rails line up. But adoption should still be measured carefully. Use official source dates, and avoid mixing cumulative report metrics with current active-use assumptions.

For B2B operators, the business side of Toss may be just as important as the consumer app. Checkout, payments, financial dashboards, and POS-style tools show that Toss is also competing for the merchant operating layer.

FAQ

Is Toss the same company as Viva Republica?

Toss is the consumer-facing brand and app ecosystem. Viva Republica Inc. is the company behind Toss. Related services such as Toss Bank, Toss Securities, Toss Payments, and Toss Place may have their own public surfaces, operating entities, or disclosure paths.

Why is Toss called a fintech super app?

Toss is called a super app because it brings many financial tasks into one experience: spending management, transfers, credit scores, loans, investing, payments, insurance, business tools, and more. The strategic point is not just the number of features, but the habit of using one interface for many financial decisions.

How popular is Toss in Korea?

Toss's official team page says the service is used by more than one in two Koreans and provides age-group registered-user figures based on December 2024 data. For any commercial analysis, distinguish registered users from active users, transaction volume, and revenue.

Can overseas fintech companies copy Toss?

They can learn from Toss, but they should not copy it blindly. Korea's digital finance habits, regulatory environment, consumer expectations, and partnership rails are specific. The more transferable lesson is to start with a frequent trust-heavy problem, then expand only after the product earns habit and credibility.

What is the biggest risk in the Toss model?

The biggest strategic risk is complexity. As Toss expands across banking, securities, payments, insurance, merchant tools, advertising, and data-driven recommendations, it must keep user trust, compliance quality, and product clarity intact.

Sources And Further Reading

More Business Guides

MUSINSA Deep Dive 2026: Korea's Fashion Platform Going Offline and Global

A public-info deep dive on MUSINSA, Korea's fashion platform, covering growth, offline stores, global push, brand ecosystem, and risks.

Korean Cosmetics Wholesale Guide 2026: Authorized Distributors, Gray Market Risk, and Where Buyers Should Look

A Korean cosmetics wholesale guide covering authorized distributors, gray-market risk, sourcing platforms, category checks, and documents.

Korean Packaging Suppliers: Cosmetics And Food Guide

A practical guide to Korean packaging suppliers for cosmetics, food, labels, cartons, MOQs, samples, compliance checks, and export-ready sourcing.